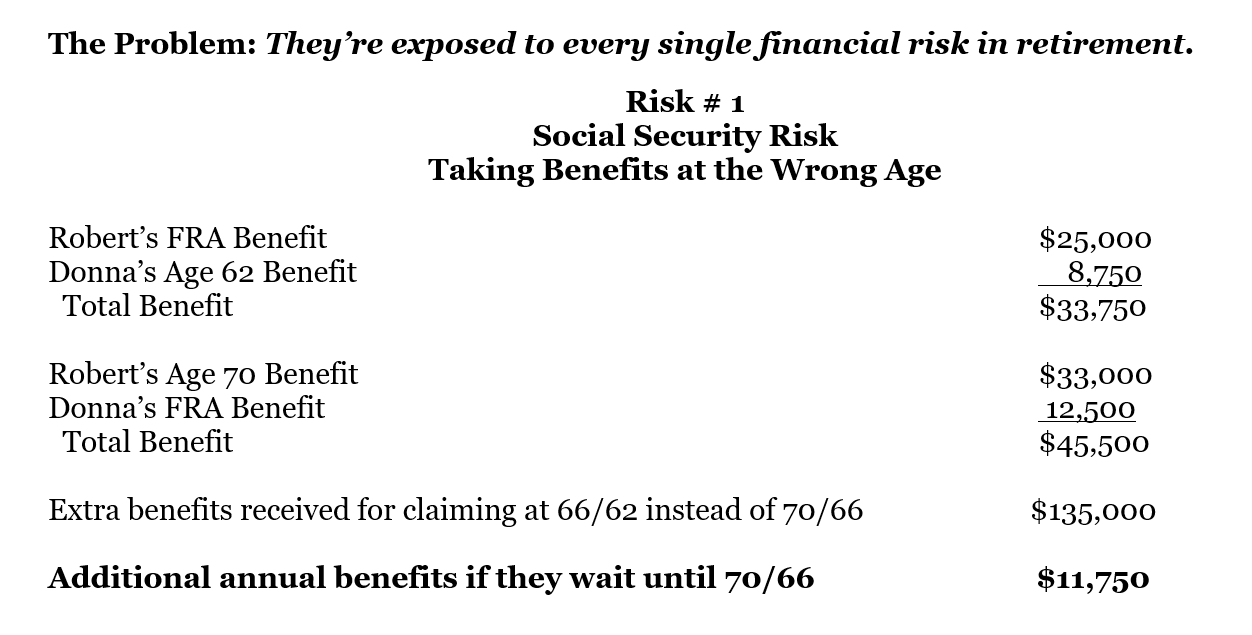

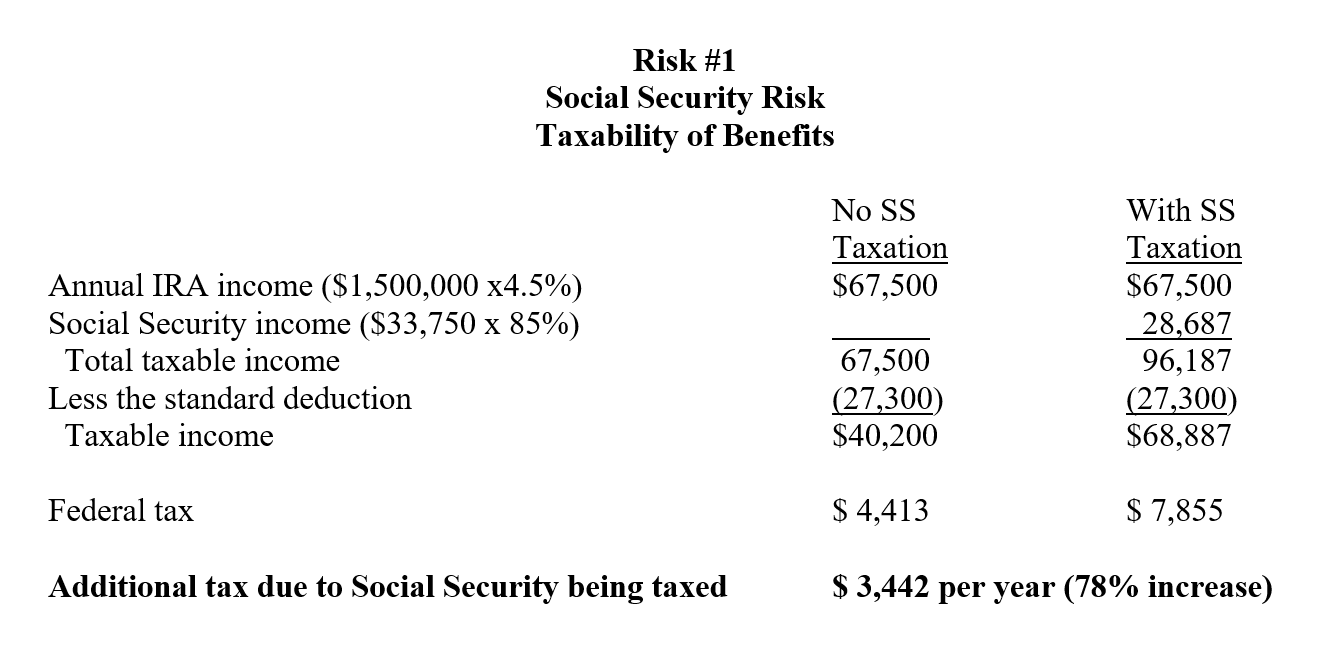

Social Security risk: The Deckers maximized their Social Security benefits by waiting until their full retirement age (FRA) to claim, and they allocated their income so that their Social Security is not taxed.

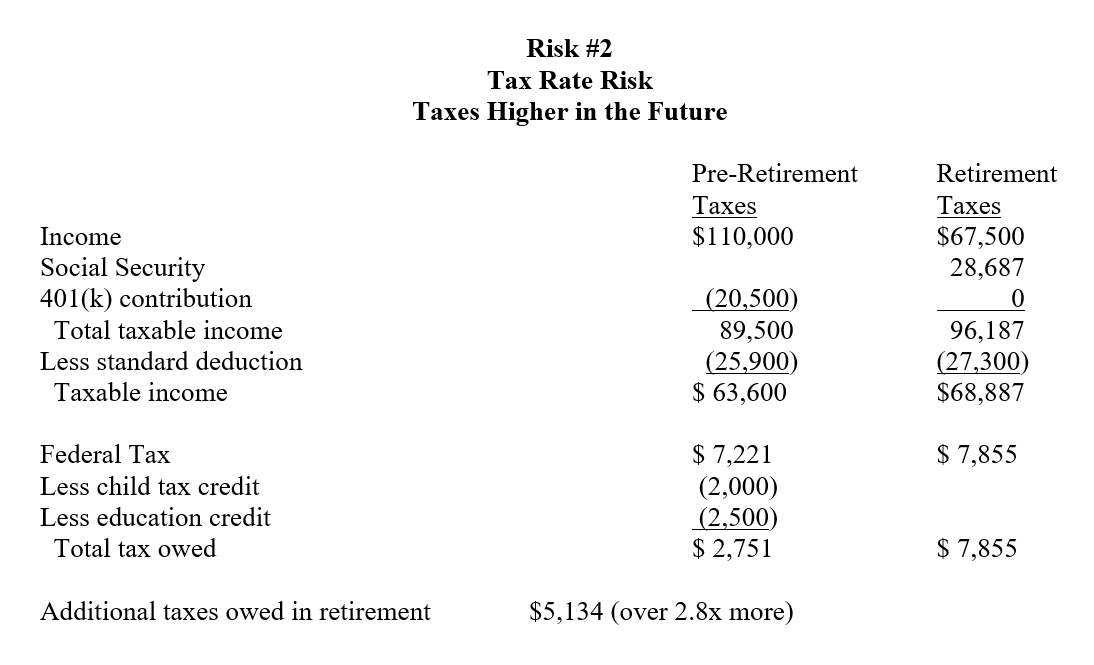

Tax rate risk: The Deckers have no taxable income under their current plan.

Longevity risk: They can enjoy a long life because they have guaranteed income from Social Security and an annuity that will never run out.

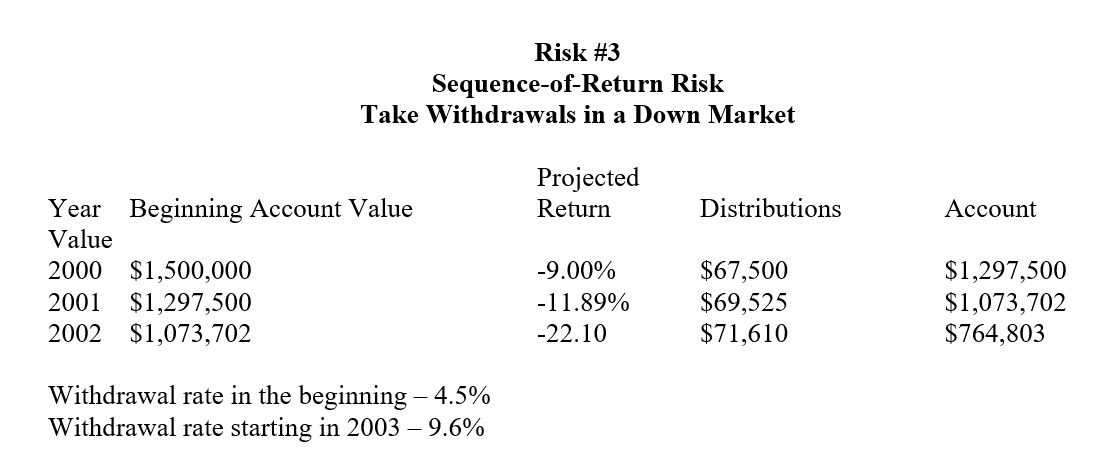

Sequence of return risk: The market can go up and down, but it will not impact Robert and Donna’s daily lifestyle because their annuity income is guaranteed. The only assets they have at risk are what is left in their taxable, tax-deferred, and Roth IRA buckets, and these assets are not required for their daily living expenses.

Withdrawal rate risk: The Deckers’ withdrawal rate has been set as part of their financial plan. They can get an above-average withdrawal rate because some of their assets have principal protection.

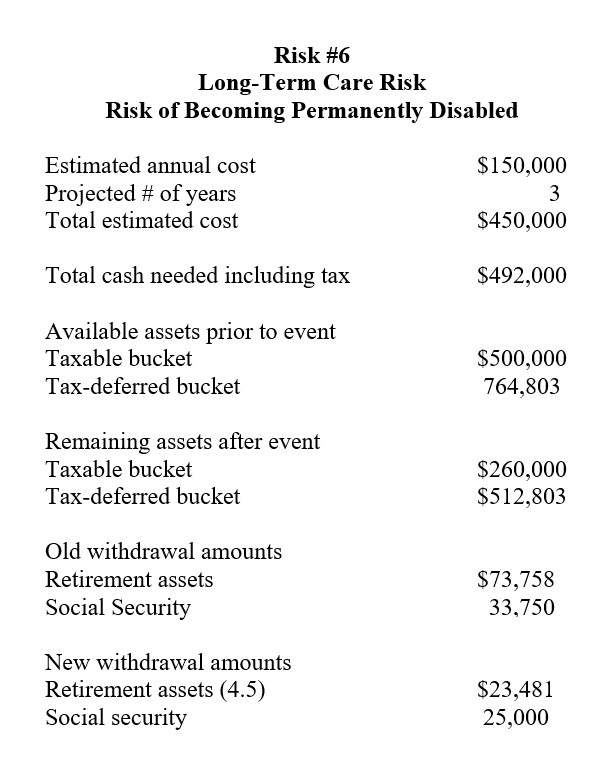

Long-term care risk: If they need long-term care, they can activate the chronic illness rider on their life insurance policies. This will allow them to access the death benefit early to help cover the cost of long-term care.

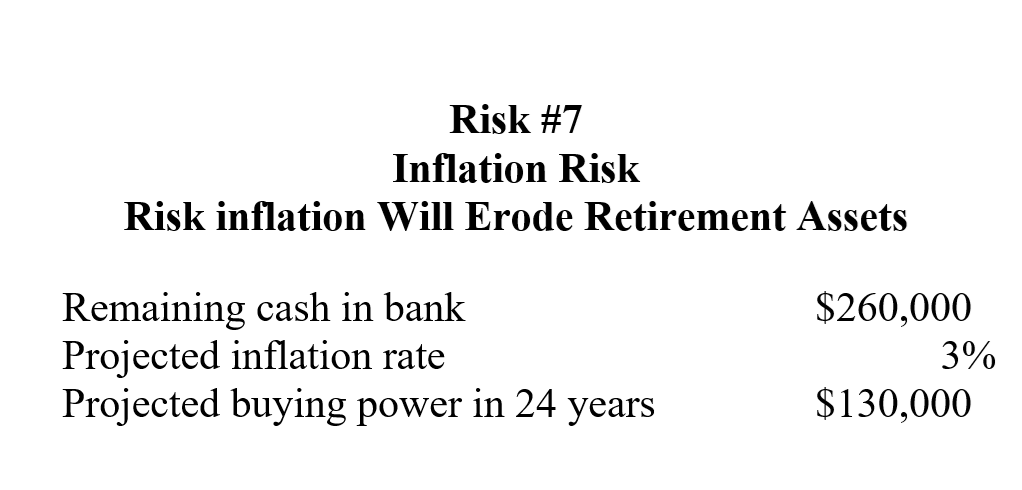

Inflation risk: They have inflation-adjusted Social Security and an inflation-adjusted annuity. Their annuity payments will increase as the annuity value increases due to investment growth.

Medicare risk: The Garcias are happy with their Medicare Advantage Plan, but they check it each year to make sure there are no changes to their coverage. If they find changes they are not happy with, they will consult with a broker to look for other alternatives.

Elder abuse risk: This risk has been reduced because they have a plan in place to cover their financial needs throughout their retirement. Donna has the income and structure she needs to maintain her lifestyle even Robert was to pass away early due to complications from a long-term care event.

Lack of income diversity risk: By having four sources of tax-free income, the Deckers are in a great position to continue to manage the financial risks facing their retirement.